Brown's Triple Exponential Smoothing is implemented on data showing a quadratic trend over time. It works well for data that has a very steep growth or decline. The Brown's Triple Exponential Smoothing method attempts to create a linear equation by performing three simple exponential smoothing forecasts and then adjusting for the linear trend in the data. The smoothing constant in this model should be chosen between .02 and .11. Triple Exponential Smoothing can forecast multiple time periods into the future.

To use the Triple Brown Forecasting technique:

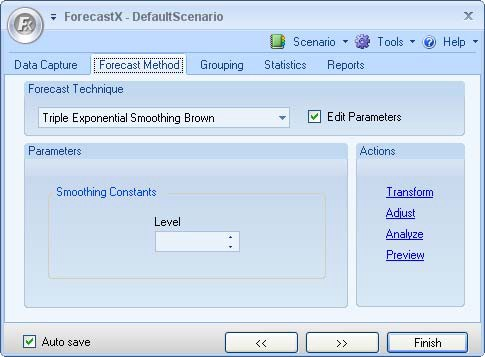

- Click on the Forecast Method tab.

- In the Forecast Technique area, scroll through the list of methods and select Triple Brown. The Triple Exponential Smoothing Brown Forecasting technique displays.

-

Select Edit parameters to activate Triple Brown’s parameters.

-

In the Smoothing Constants area, type in a number of levels.

- Click Finish.